Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

All voices matter

In today’s financial landscape, investment funds have become a go-to option for both novice and experienced investors looking to grow their wealth without diving into the complexities of picking individual stocks or bonds. Drawing from years of watching market trends and advising on portfolios, I’ve seen how these vehicles can simplify investing while offering diversification and professional oversight. But what exactly are they, and how do they function in practice? This guide cuts through the noise, explaining the essentials with real-world insights to help you decide if they’re right for your strategy. Whether you’re building a retirement nest egg or seeking steady income, understanding investment funds could be the key to smarter decisions.

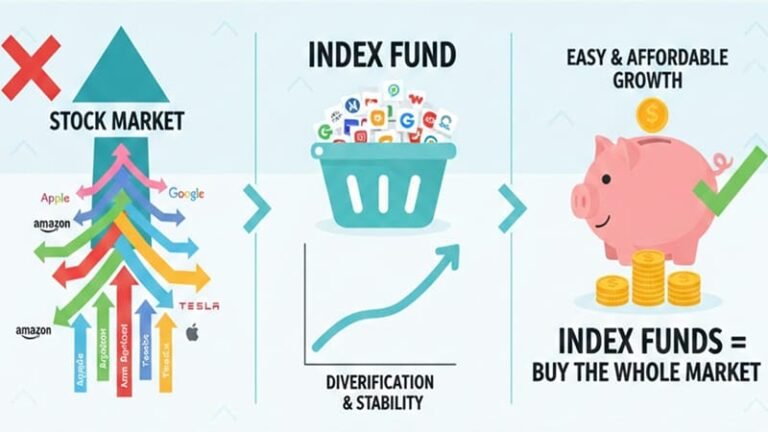

At their core, investment funds pool money from multiple investors to buy a diversified mix of assets like stocks, bonds, real estate, or even commodities. This collective approach lets everyday people access opportunities that might otherwise require massive capital or expertise. Think of it as joining a group buy—everyone chips in, and a professional manager handles the details to aim for returns while spreading out risks.

Unlike buying a single stock, where your fate ties to one company’s performance, funds spread investments across dozens or hundreds of holdings. This setup emerged centuries ago, with roots in the Dutch Republic in the 1700s, but modern versions like mutual funds kicked off in the 1920s with the Massachusetts Investors Trust. Today, they’re regulated heavily to protect investors, ensuring transparency on holdings, fees, and performance.

Funds come in various flavors, but they all share a common goal: generating returns through capital appreciation, dividends, or interest. The net asset value (NAV)—essentially the fund’s total assets minus liabilities, divided by outstanding shares—determines your share price. It’s recalculated daily for most funds, reflecting the underlying investments’ worth.

Not all investment funds are created equal. They vary by structure, strategy, and accessibility, each suiting different risk tolerances and time horizons. Here’s a breakdown of the main categories to help you navigate.

To make this clearer, check out this comparison table of popular fund types based on structure, liquidity, and typical costs:

| Fund Type | Structure | Liquidity | Typical Fees (Expense Ratio) | Best For |

|---|---|---|---|---|

| Mutual Funds | Open-end | Daily at NAV | 0.5%–1.5% | Long-term growth, diversification |

| ETFs | Exchange-traded | Intraday on exchanges | 0.03%–0.5% | Cost efficiency, quick trades |

| Hedge Funds | Private, often leveraged | Limited, lock-up periods | 1%–2% + performance fees | High-risk, high-reward strategies |

| Closed-End Funds | Fixed shares | Market-dependent | 0.5%–1% | Potential discounts to NAV |

| Money Market Funds | Open-end, short-term debt | High, daily | 0.1%–0.5% | Preserving capital, liquidity |

This table highlights why ETFs often win for beginners—lower costs and flexibility—while hedge funds appeal to those comfortable with complexity.

The mechanics start with investors buying shares or units in the fund, contributing to a collective pot. A fund manager—backed by a team of analysts—then deploys this capital according to the fund’s prospectus, which outlines goals, risks, and strategies. For active funds, this means researching and trading securities to beat the market. Passive ones simply replicate an index, minimizing decisions and costs.

Returns come in two main forms: income from dividends or interest, distributed periodically, and capital gains when the fund sells assets at a profit. You might receive these as cash or reinvest them for compounding growth. Fees eat into returns, including management expenses (often 0.5%–2% annually), sales loads (upfront or back-end charges), and transaction costs from portfolio turnover.

Regulation plays a big role. In the U.S., the Investment Company Act of 1940 oversees most funds, mandating disclosures via prospectuses and quarterly reports. Globally, frameworks like Europe’s UCITS ensure cross-border standards. Risks? Market volatility can tank NAV, interest rate shifts hurt bond funds, and liquidity issues arise in stressed times, as seen in 2020’s pandemic dips.

Investment funds shine in accessibility. They offer instant diversification—reducing the sting if one holding flops—and professional management, saving you hours of research. Economies of scale mean lower per-person costs, and options like tax-advantaged funds in IRAs add appeal.

On the flip side, you surrender control over specific picks, and fees can accumulate, eroding gains over time. Active funds often underperform indexes after costs, and locked-in periods in private funds limit flexibility. Plus, no guarantees—principal loss is always possible, especially in equities.

In my experience, the pros outweigh cons for most, particularly if you match the fund to your horizon. Short-term needs? Stick to money markets. Long-haul growth? Equities or mixed funds.

Selecting a fund isn’t guesswork. Start with your goals: income for retirees, growth for young professionals? Assess risk tolerance—can you stomach 20% drops? Review the prospectus for strategy, past performance (though not predictive), and fees via tools like FINRA’s Fund Analyzer.

Compare benchmarks: Has it beaten its index consistently? Factor in taxes—hold in retirement accounts to defer hits. Diversify across fund types, and rebalance annually. For beginners, low-cost index ETFs like those tracking the S&P 500 are hard to beat, offering broad exposure without the hype.

Investment funds democratize wealth-building, turning small sums into powerful portfolios through pooling and expertise. They’ve evolved from niche tools to trillion-dollar mainstays, adapting to trends like sustainable investing and digital platforms. If you’re ready to invest without going solo, start small, educate yourself, and consult a advisor if needed. The right fund could accelerate your financial journey—just remember, patience and due diligence pay off in the end.