For forty years, the global economy has been fueled by a specific demographic fluke: the American Baby Boomers. Born between 1946 and 1964, this generation didn’t just witness the greatest asset super-cycle in history—they were the super-cycle.

However, as we approach 2026, the mechanics of wealth are shifting from accumulation to forced distribution. This isn’t a “market choice”; it is a systemic reset governed by actuary tables and the Internal Revenue Service (IRS).

End of the Goldilocks Era

The 2026 “Red Line”: Why Now?

While wealth transfer is a gradual process, 2026 acts as a physical barrier for two reasons:

The Pension Floor: On January 1, 2026, the youngest Boomers turn 62, the minimum age for Social Security. This marks the total exit of the most productive and wealthiest labor force in history.

The Mortality Peak: The “leading edge” Boomers (born 1946), including figures like Donald Trump, will enter their 80s. According to U.S. Census Bureau actuarial data, this is the statistical “peak zone” for mortality.

The Composition of the $84 Trillion

Segment

Amount

Primary Asset Class

Status

Silent Generation

~$25–30 Trillion

Real Estate / Cash

Active Transfer (Ages 81–98)

Baby Boomers

~$53+ Trillion

Equities / 401(k) / Business Equity

Entering Peak Liquidation

Total Transfer

$84 Trillion

Diversified

20-Year Window

The “Automatic Seller”: How Law Forces the Hand of the Market

Many investors believe Boomers will simply “hold” their stocks forever. US tax law says otherwise.

1. The RMD Trap (Required Minimum Distributions)

The IRS does not allow tax-deferred wealth to sit forever. Once an individual hits 73, they are legally required to withdraw a percentage (roughly 4%) of their 401(k) and IRA assets annually. Failure to do so results in a staggering 25% excise tax.

The Impact: The wealthiest Boomers (born 1950–1952) have just crossed this threshold. We are looking at hundreds of billions in mandatory equity sales every December, regardless of market conditions.

2. IRS Code Section 1014: The “Step-Up in Basis”

This is the “Sell Trigger” for heirs. If a parent buys a stock for $1M and it grows to $60M, selling it before death incurs a massive capital gains tax. But upon death, the “cost basis” resets to the current market value.

The Heir’s Logic: An heir can sell $60M of stock the day after the funeral and pay zero capital gains tax. This creates a massive, rational incentive for the “Prince Charles Generation” (heirs aged 50–60) to liquidate inherited portfolios immediately.

The Political Theater: Trump, Crypto, and the “Landing Strip”

The return of Donald Trump to the presidency in 2025 is not a coincidence of populism; it is a functional requirement for “Old Money” seeking a safe exit. The 2026–2030 window requires a specific policy “cocktail” to keep the $84 trillion from evaporating during the transfer:

Tariffs & Deregulation: These are designed to artificially inflate corporate margins and prop up the stock market, ensuring Boomers sell at “All-Time Highs.”

The Crypto Sponge: Trump’s pivot to Bitcoin serves a vital purpose. To prevent $84 trillion of “moving money” from hyper-inflating the price of bread and rent (CPI), the administration needs a “monetary sponge.” Crypto absorbs trillions in liquidity, locking inflation into digital assets rather than the real-world economy.

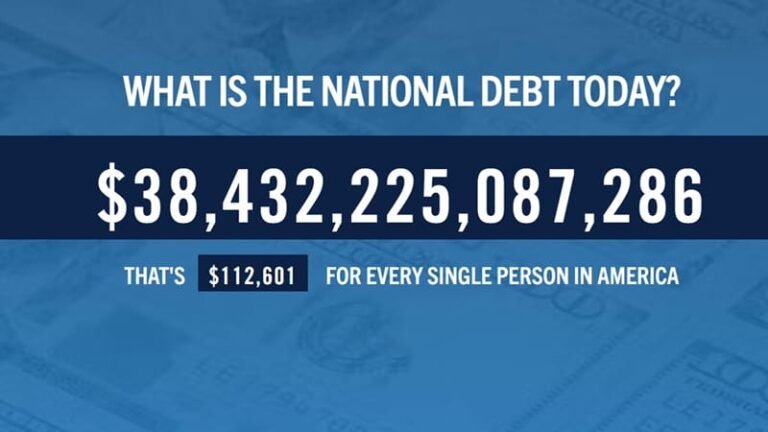

Debt Dilution: With $36 trillion in national debt, the U.S. cannot “pay” its way out. It must “inflate” its way out. By maintaining a “high-inflation, high-growth” environment, the real value of the debt shrinks while the nominal price of the stock market stays high.

The Survival Guide: Who Wins?

We are moving into a “De-stocking Crisis” for financial assets. As the supply of stocks from estates increases, the traditional “buyer” (the middle class) is too debt-burdened to absorb them.

The only entities left to buy are:

Corporations: Engaging in massive share buybacks (exceeding $1 trillion annually by 2025) to prevent price collapses.

The Fed: Eventually, the Federal Reserve will be forced to engage in “Socialized Equity Support”—printing money to keep the pension-linked stock market from hitting zero.

Strategic Takeaways for 2026:

Volatility is the New Beta: The 40-year era of “Low Vol / High Return” is dead. We are entering an era of “Inflationary Bull Markets”—where the index goes up, but the purchasing power of the currency goes down.

The Heir Effect: Watch for “firing the advisor” trends. As Gen X and Millennials fire their parents’ traditional wealth managers, expect a massive rotation from “Value” stocks into “Growth,” “Tech,” and “Alternative” (Crypto) assets.

Final Thought

The approximately $84 trillion in legacy capital is withdrawing from the market. Its objective is to avoid losses; however, losses are unavoidable, which means the cost must ultimately be borne by others. In this unprecedented transfer of wealth, only two categories of participants are likely to endure: those with billions of dollars who shape the rules of the game, and those who possess a clear understanding of those rules.