Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

All voices matter

The financial world is currently intoxicated by a “soft landing” narrative. Markets are flirting with all-time highs, inflation appears to be cooling, and the collective memory of 2008 has faded into a historical footnote. But while the masses chase the tail-end of a liquidity-driven rally, Jim Rogers—the man who co-founded the Quantum Fund and anticipated the 1987 crash and the 2000 dot-com bust—is sounding a clarion call that sounds less like a prediction and more like a mathematical certainty.

His thesis for 2026 is simple yet chilling: In 2008, we saved the banks. In 2026, there will be no one left to save the states.

To understand why the next crisis will be “the worst in a lifetime,” we must look at where the rot currently resides. In 2008, the crisis was systemic but localized within the private sector—specifically subprime mortgages and over-leveraged investment banks.

The solution back then was a massive “risk transfer.” Central banks slashed interest rates to zero and governments moved private toxic debt onto public balance sheets. This worked for a decade because inflation was dead and globalization provided a massive tailwind. Today, that safety net has become the trap.

| Metric | 2008 Crisis Context | 2026 Projected Reality |

| Primary Risk Location | Private Banks / Shadow Banking | Sovereign States / Central Banks |

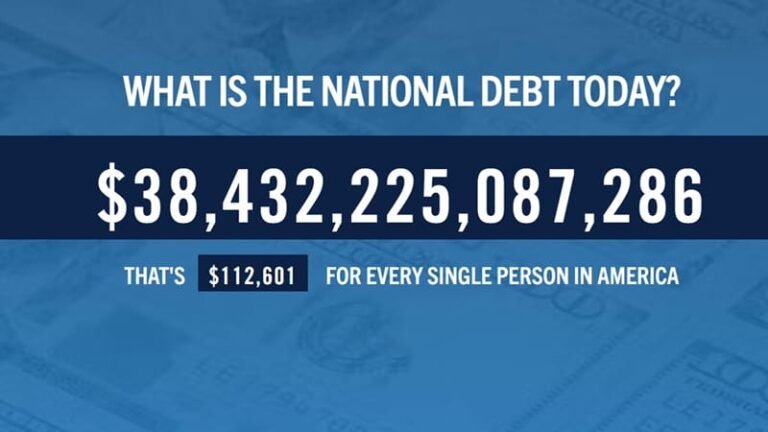

| US Debt-to-GDP | ~64% | ~124% |

| Interest Rate Environment | High (Room to cut) | High (Stuck due to sticky inflation) |

| Global Debt Total | $142 Trillion | ~$315+ Trillion |

| Primary “Firefighter” | Federal Reserve / Treasury | Diminished (Limited Policy Space) |

The most significant shift since 2022 isn’t just that rates went up; it’s that the cost of carry for nations has fundamentally decoupled from their ability to tax.

For years, the US and Japan operated under the “Modern Monetary Theory” (MMT) delusion: that debt doesn’t matter as long as you print the currency. However, as Rogers points out, the return of inflation destroyed this paradigm. When the US 10-year yield sits above 4%, the interest expense on $36 trillion in debt starts to exceed the national defense budget.

Rogers frequently highlights Japan as the “canary in the coal mine.” With a debt-to-GDP ratio exceeding 260% and a shrinking, aging population, Japan is a laboratory for sovereign collapse. If the Bank of Japan allows rates to rise to fight inflation, the government goes insolvent. If they keep rates low to fund debt, the Yen collapses. This “checkmate” position is what Rogers believes will eventually migrate to the West.

A pillar of the 2026 thesis is the fracturing of the dollar-centric world order. For 80 years, the US could export its inflation and debt because the world had no alternative.

We are now seeing a structural shift:

When the “risk-free asset” (US Treasuries) begins to be questioned, the discount rate for every other asset class—stocks, real estate, private equity—goes into chaos.

Jim Rogers isn’t a “permabear” who hides in a bunker; he is a pragmatist. His current positioning reflects a pivot from growth-seeking to resilience-building.

Rogers has long advocated for commodities—agriculture, silver, and gold. Unlike a government bond, a bushel of wheat or an ounce of silver cannot be printed into oblivion. In a sovereign debt crisis, “counterparty risk” becomes the primary concern. Gold is the only financial asset that is not someone else’s liability.

In 2008, the “dash for cash” caused everything to sell off initially. Rogers emphasizes holding “real” liquidity. This doesn’t necessarily mean just USD, but rather the ability to remain solvent when markets freeze.

One of Rogers’ most controversial takes is his move to Asia and his skepticism of the “Western Century.” He argues that capital will naturally flow to jurisdictions that are net creditors rather than net debtors.

Financial crises rarely happen because of a single data point. They happen when a long-held “myth” dies. The myth of the last 15 years was that governments can borrow infinitely without consequence. By 2026, the convergence of record-high debt, structurally higher interest rates, and geopolitical fragmentation will likely force a reality check. Whether it’s a “Lehman moment” for a G7 nation or a slow-motion devaluation of currencies, the era of “easy bailouts” is over.

As an investor, your goal isn’t to predict the exact Tuesday the market drops; it’s to ensure that when the “firefighters” (the states) are the ones on fire, you aren’t standing in the same building.